The GLP-1 Boom That’s Reshaping Pharma

From blockbuster margins to price pressure, GLP-1 is rewriting pharma economics.

GLP-1 has become one of the most valuable drugs in modern medicine. Originally developed to treat type 2 diabetes, it has since unlocked a multi-billion-dollar weight loss market. The first GLP-1 drug, Byetta (exenatide), launched in 2005 through a collaboration between Amylin Pharmaceuticals and Eli Lilly to help people with type 2 diabetes by mimicking a natural hormone that regulated blood sugar by stimulating insulin release and slowing digestion.i

The defining shift came after its original use case. Over time, researchers and doctors began noticing that patients were consistently losing weight, largely because the medicines reduced appetite and increased feelings of fullness. That observation shifted how GLP-1s were positioned. What began as a diabetes treatment quickly became one of the most effective tools in obesity care, with clinical trials confirming significant weight loss even in non-diabetic patients.

The Market Explodes

The market took off when Novo Nordisk’s semaglutide entered the obesity space as Wegovy in 2021, following the earlier launch of Ozempic for diabetes in 2018.ii For the first time, a drug could deliver around 15% weight loss, something medicine had not achieved at scale with either pills or injections ever before.

Demand surged quickly, particularly in the US where obesity rates are high. Novo’s stock price jumped around 7% in a single day and that was just the beginning. Eli Lilly was not far behind. While it had already launched Mounjaro for diabetes in 2022, it formalised its position in the weight loss market with Zepbound in 2023. Together, the two companies came to dominate the space.

The economics were compelling. GLP-1 drugs were priced at roughly $1,350 per month, or over $16,000 per year, even before insurance adjustments. Prescriptions grew by nearly 588% between 2019 and 2024, while bariatric surgeries fell by 42% over the same period.iii

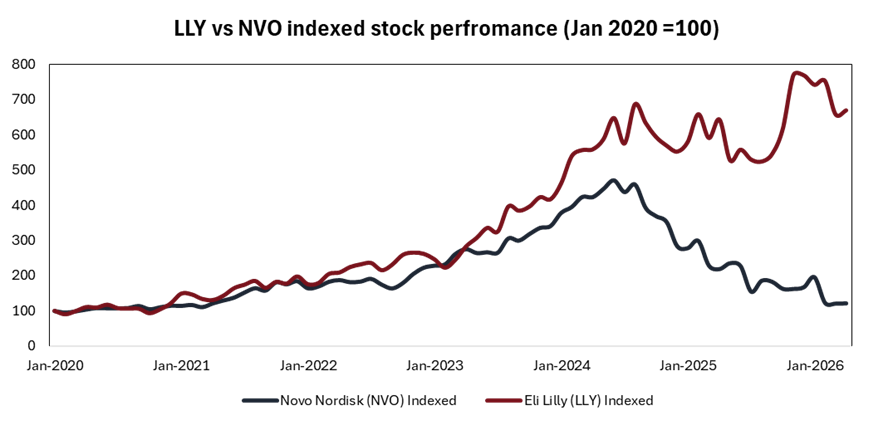

By mid 2024, Novo Nordisk had become Europe’s most valuable listed company, reaching a market cap of around $425 billion after gaining more than 250% in five years and overtaking French luxury retailer LVMH. Lilly followed closely, with its shares rising roughly 59% in 2023 on the back of strong demand for Mounjaro and Zepbound.

Novo remained the market leader until it all started to unravel in late 2024. Trial results showed that Lilly’s Zepbound delivered greater weight loss than Wegovy, shifting momentum in the category. To add to the pressure, Novo’s next-generation candidate CagriSema underwhelmed, delivering 22.7% weight loss in a late-stage trial against expectations of 25%.

The impact was swift. Within six months, Novo lost around 30% of its value and began ceding market share to Lilly. By late 2025, Lilly reached a $1 trillion market capitalisation, becoming the first healthcare company to enter a club largely dominated by tech firms. iv

The Rise of Compounding Pharmacies

Novo began losing share not only to Lilly, but to compounding pharmacies (‘compounders’). Unable to meet demand for semaglutide due to supply constraints, the company left a gap that compounders quickly moved to fill at scale.

These pharmacies found ways to operate within regulatory grey areas by slightly altering formulations of what were still essentially semaglutide-based GLP-1 drugs. Additions such as B vitamins or levocarnitine were positioned as offering weight loss support or energy benefits. By October 2025, semaglutide and tirzepatide made up over 80% of compounded GLP-1 supply, highlighting how concentrated the market had become.

Despite warnings from the FDA, compounders continued operating, bridging the demand-supply gap while offering far lower prices to patients. A number of platforms scaled rapidly, including Hims & Hers, Ro, LifeMD, WeightWatchers, Noom, Calibrate, Sesame, Teladoc, and 23andMe.

Novo’s response was pragmatic. It partnered with Hims & Hers, LifeMD, and Ro to distribute authentic Wegovy through those platforms at around $499 per month. In effect, it pulled the largest compounders into the regulated supply chain. If you can’t beat ‘em, join ‘em, as the adage goes. Lilly took a similar approach with LillyDirect, although it has been less exposed to compounding given that tirzepatide is more complex to manufacture than semaglutide.

Prices Start to Slide

The rise in competition has significantly driven down the price of GLP-1 drugs and made them more accessible to a broader market. Pricing is also being shaped by country-specific regulation and government intervention.

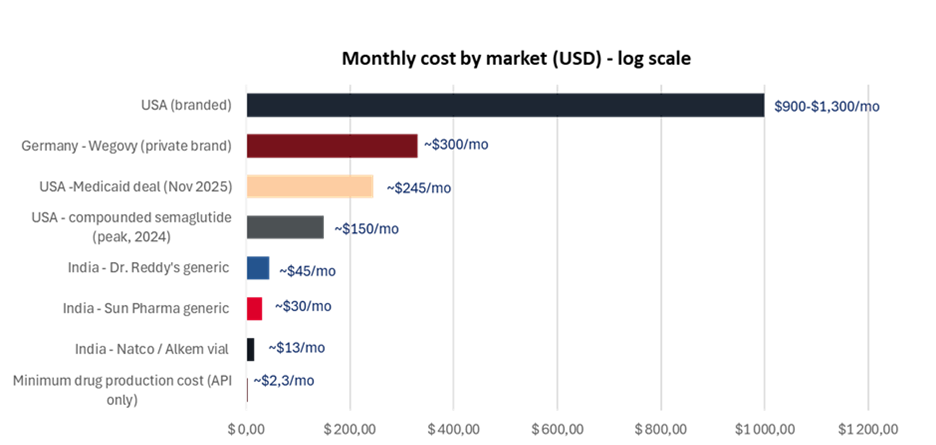

In Germany, a statutory pricing negotiation framework known as AMNOG requires pharmaceutical companies to justify drug prices against clinical benefit within months of launch. The government’s health insurance body then negotiates a national reimbursed price. In practice, this has brought Wegovy down to around €300 per month – roughly a third of the US list price – driven by policy rather than pricing discretion.

In the US, the November 2025 Medicare agreement reduced the government-covered price to around $245 per month, broadly in line with German levels. vi That said, this pricing applies only to Medicare and Medicaid enrollees, not the broader commercial market.

At the same time, compounders continue to undercut branded drugs. While technically restricted from large-scale production, platforms such as Hims & Hers are offering compounded semaglutide for around $99 per month, keeping downward pressure on prices.

Generics: The Race to Beat the Patents

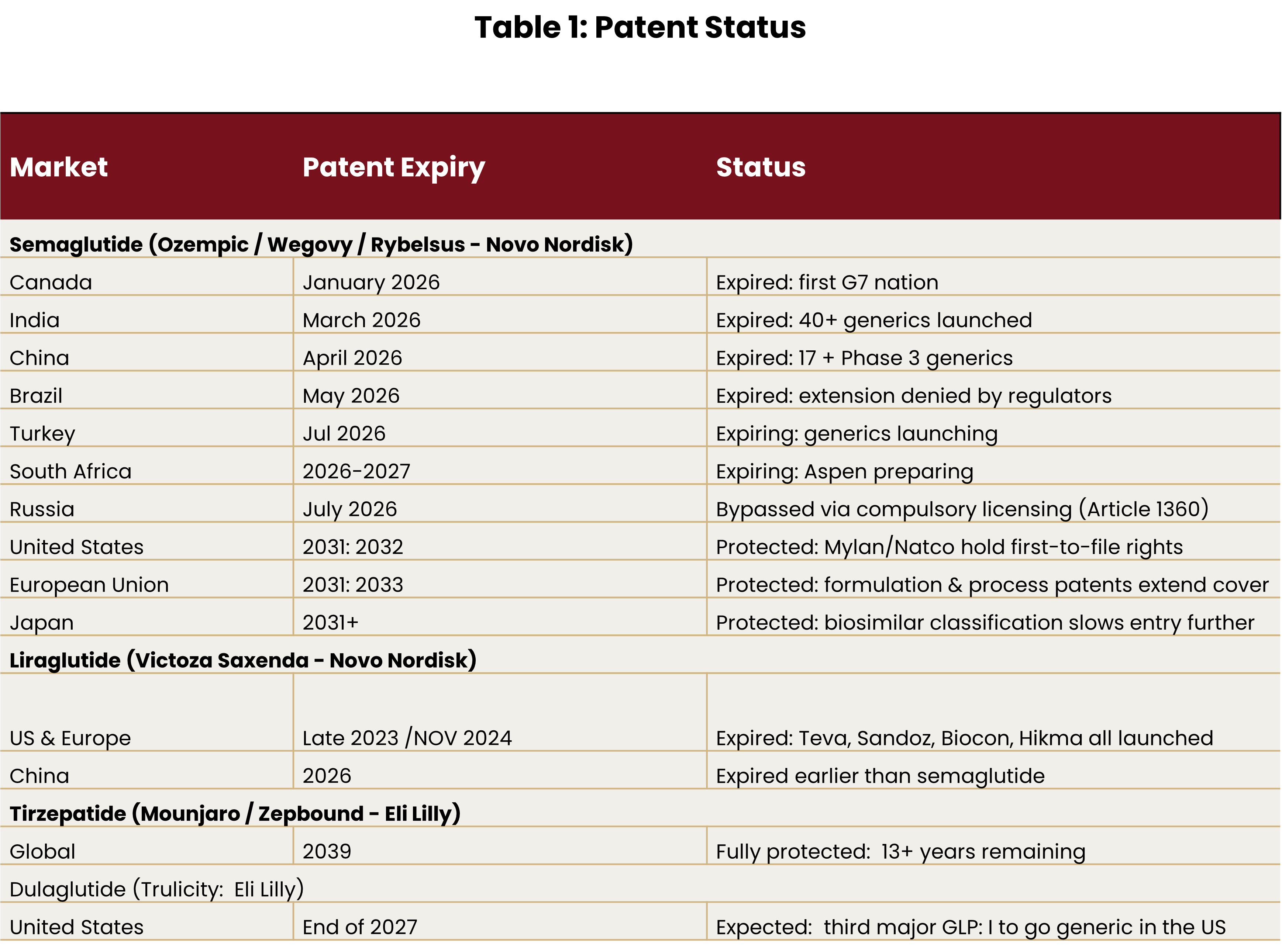

With semaglutide’s patent having expired in March 2026, competitive pressure is far from easing. Several players are preparing to launch generic GLP-1 drugs, opening a new front in the market. vii The focus now shifts to supplying lower-cost alternatives to the millions of patients who have been priced out until now.

Some early movers have already launched, while others are in advanced stages of bringing generic GLP-1s to market. Companies such as Natco Pharma, Sun Pharmaceuticals, and Dr. Reddy’s have introduced generics at significantly lower prices, often 70% to 80% below branded alternatives.

Several others are close behind, including South Africa’s Aspen Pharma. The company has already entered the GLP-1 market through a distribution agreement with Lilly for Mounjaro in Southern Africa, but its ambitions extend further. Aspen is positioning itself to be a meaningful player in generics.

For manufacturers, success will depend on execution rather than breakthrough innovation. The winners will be those that move quickly through regulatory approvals, target the right markets, and deliver at a competitive price with credible quality. Aspen has leaned into that approach, registering GLP-1 drugs in markets where patents are nearing expiry.

Canada is its first target – a strategically important move given that Canadian regulatory approval is widely used as a quality benchmark in other markets. Aspen is targeting approval between May and September 2026, which would position it among the first companies to bring a credible generic to a G7 country.

Manufacturing is being set up across two facilities: one in France to support European regulatory credibility, and one in South Africa to anchor local production. Aspen plans to price its generic at less than half the global branded price, a move that could materially expand access across Africa and other emerging markets.

Looking at the patent expirees, it’s clear that more players are coming for Novo’s lunch, while Lilly remains protected into the early 2030s. But Novo is not going down without a fight.

The company has already cut prices for Wegovy and Ozempic to $349 per month for cash-paying patients, filed a new drug application for CagriSema in December 2025 to improve efficiency, and launched an oral version of Wegovy. It is also advancing Amycretin, a next-generation treatment targeting both GLP-1 and amylin receptors, available as a once-weekly injection or oral option.viii Novo’s CEO has expressed confidence in oral Wegovy’s competitive position, citing clinical trial data that suggests it can deliver weight loss comparable to its injectable version.

Lilly is not standing still either. Its oral pill, Foundayo (orforglipron), received FDA approval in April 2026. One practical advantage over Novo’s offering is the lack of dietary restrictions. Novo’s pill must be taken with no more than four ounces of water, followed by a 30-minute fast before eating or drinking. It may seem like a small detail, but for many patients, it matters.

What Comes Next for the Market, and Who Wins?

Looking at the patent timeline, branded drugs are likely to remain dominant in the US and Europe for several more years. Lilly appears well positioned to lead, with a more effective drug and a small but meaningful advantage in its oral offering.

Novo has warned that sales could fall by 5% to 13% in 2026, a sharp reversal for a company that was recently Europe’s most valuable. At the same time, price pressure from compounders and government intervention is expected to persist, which will likely weigh on margins even in these premium markets.

In emerging markets, price deflation has already begun, with several Indian generics entering the market. Manufacturers in China and Brazil are also preparing to launch as patents expire.

Over the next few years, these drugs are likely to shift from premium treatments for wealthier patients to more accessible options for hundreds of millions across the developing world. In Africa, Aspen stands out as the company to watch. It is perfectly positioned to manufacture its own generics, leverage its existing distribution infrastructure across the continent, and serve both local and broader emerging markets at a price point that could unlock entirely new patient groups.

Competition remains intense, even as the drugs themselves continue to improve. Lilly and Novo are still defending their market positions, but the market is expanding rapidly. The GLP-1 market was worth around $70 billion in 2025. Forecasts vary on how large it will become, but the direction is clear: this is a market that is still growing, and everyone wants a piece.

Who wins? Lilly looks like the frontrunner for now. Its drug is more effective, its pipeline is stronger, and its patent protection on tirzepatide runs through 2039.

But the story does not end there. Novo is pushing back with new formulations and a next-generation pipeline. At the same time, the rise of generics is reshaping the competitive landscape.

Over the longer term, the real winners may be the patients in India, Brazil, South Africa, and across the developing world who will gain access to medicines that, until very recently, were out of reach. In that sense, the GLP-1 revolution is only just beginning.

iUSFood & Drug Administration. Byetta (exenatide) — Drug Approval Package.NDA 021773, approved 28 April 2005. Amylin Pharmaceuticals / Eli Lilly andCompany.

iiUS Food & Drug Administration. FDA approves new drug treatment for chronicweight management. NDA 215256 (Wegovy,semaglutide injection 2.4 mg), approved 4 June 2021.

iiiFairHealth. GLP-1 Receptor Agonist Prescriptions for Weight Loss, 2019–2024. 2025./ PharmExec: Orforglipron and Retatrutide Named as Defining GLP-1 Drugs of the NextDecade. Citing Fair Health 2025 data.

ivCNBC.Eli Lilly hits $1 trillion market value, a first in health care, as NovoNordisk tumbles. 21 November 2025.

vHealthcareBrew. Despite FDA crackdown, unapproved GLP-1s still threaten the industry.March 2026. Citing IQVIA October 2025 report on compounded GLP-1 prescriptions

viPrimeTherapeutics. GLP-1 Pipeline Update: November 2025. Detailsthe November 2025 CMS agreement setting Medicare GLP-1 prices at $245/month.

vii GeneOnline.The 2026 GLP-1 Patent Cliff: Generics, Global Competition, and the $100Billion M&A Race. March 2026. / CNBC. India is launching cheap weight-loss drugs. 23March 2026.

viiiNovo Nordisk. Novo Nordisk files for FDA approval ofCagriSema. Press release, 18 December 2025. / Eli Lilly. FDA approves Foundayo (orforglipron). 1April 2026.