.png)

When it comes to investing, some voices cut through the noise with rare clarity. One of them belongs to Howard Marks, co-founder and co-chairman of Oaktree Capital Management. In a world obsessed with the next big thing, his steady message about value, price and patience is both refreshingly simple and powerfully relevant – especially when the data tells a story that defies conventional wisdom. Marks, the largest investor in distressed securities worldwide, is famously quoted as saying, “It’s not what you buy that matters – it’s what you pay for it.” Marks’s memos, which are posted on the Oaktree website, are essential reading for serious investors. Blending sharp insight with understated wit, these letters distil decades of hard-earned wisdom into accessible reflections on risk, value and investor behaviour.

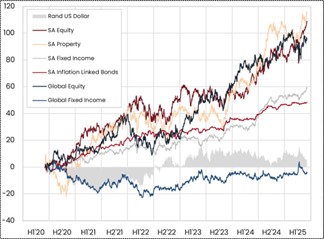

This brings us to the topic at hand: asset classes for typical multi-asset products. Contrary to conventional wisdom – and perhaps to many investors’ expectations – domestic equity and property have outperformed global equity (as measured by the MSCI All World Index) over the past five years. The next best returns were delivered by domestic fixed income and inflation-linked bonds. In stark contrast, global fixed income has been the clear laggard, posting negative returns in rand terms over the same period.

How can this be? For years, investors have been told that offshore exposure is the key to growing their retirement savings. This has been a constant siren song, and the message resonates easily in South Africa, where negative headlines about the local economy often dominate the narrative – and, by extension, investor sentiment. Often, markets are forward-looking, local assets have already priced in the bad news. Indeed, empirical evidence suggests that markets often overreact – discounting poor outlooks too heavily and becoming overly optimistic about ostensible rosy outlooks. This is central to Howard Marks’s message and provides some clues as to why South Africa has delivered a surprisingly robust set of investment returns relative to its more illustrious offshore counterparts over the past five years.

Five years ago, during the Covid-19 pandemic, risk assets around the globe were sold off sharply, with emerging markets hit especially hard as capital rushed back to developed economies. At the time, a return to normality felt uncertain – even implausible. But return to normal we did. In hindsight, that pandemic-induced sell-off proved to be a remarkable buying opportunity, particularly in markets like South Africa, where asset prices had been heavily marked down. The deeper the discount, the greater the potential upside, and local investors who acted boldly were well rewarded.

In South Africa, almost without exception, asset valuations across the board had fallen to multi-decade lows and the outlook was near-apocalyptic with domestic risk assets priced for disaster. Meanwhile, global fixed income, considered “safe”, offered wafer-thin yields and, in many cases, guaranteed negative real returns if held to maturity. In both instances, the deciding factor for long-term success wasn’t the label on the asset class, but the price paid for it.

At Mazi Asset Management, we apply Howard Marks’s insights. His mantra, “Price is what youpay; value is what you get,” is central to how we invest. In every instance, we strive to pay less than what an asset is worth. It would therefore come as no surprise that since we launched our global multi-asset portfolios in January 2022, we didn’t rush to max out offshore exposure, despite the popular chorus suggesting that’s where returns would lie. The value we saw in South African assets was simply too compelling to ignore.

Local assets have delivered solid performance, and we believe they still hold further opportunities. In an environment where the crowd is often focused on fear, we take Marks’s advice to heart: it’s not just about what you buy – it’s about what you pay for it.